Personal Cash Flow Statement Example

Understanding personal finance becomes considerably more intuitive once financial flows cease to feel abstract or fragmented. Many individuals possess a broad awareness of their monthly income, yet far fewer are able to identify with precision how that income gradually disperses through rent, subscriptions, transportation, groceries, insurance, and the accumulation of ordinary daily expenditures. This reality explains the growing importance of a personal cash flow statement, which transforms dispersed financial activity into a coherent and readable overview of everyday financial life.

Unlike a simple budget sheet, a cash flow statement shows the real movement of money throughout the month. It reveals whether income genuinely covers expenses, how much money remains available after obligations, and whether financial habits are moving toward stability or silent imbalance.

This article explores a realistic personal cash flow statement example with believable figures, practical interpretation, and a complete explanation of how the model works in everyday life.

What Is a Personal Cash Flow Statement?

A personal cash flow statement is a financial document that tracks:

- Money coming in

- Money going out

- Remaining monthly balance

The goal is not only to monitor expenses, but also to understand financial rhythm and liquidity.

A properly structured cash flow statement helps answer important questions such as:

- Am I spending more than I realize?

- Which categories consume most of my income?

- How much can I realistically save every month?

- Is my current lifestyle financially sustainable?

- Why does money feel tighter at the end of the month?

The clarity provided by this type of dashboard often changes financial behavior more effectively than traditional budgeting alone.

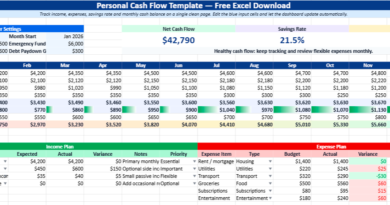

Personal Cash Flow Statement Example

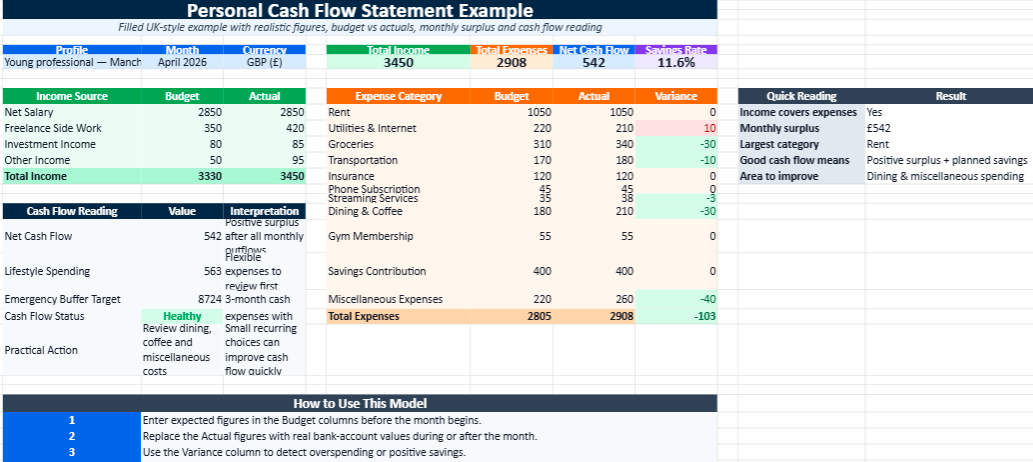

Below is a realistic monthly example based on a young professional living in Manchester.

Monthly Income

| Income Source | Amount (£) |

|---|---|

| Net Salary | 2,850 |

| Freelance Side Work | 420 |

| Investment Income | 85 |

| Other Income | 95 |

| Total Monthly Income | 3,450 |

Monthly Expenses

| Expense Category | Amount (£) |

|---|---|

| Rent | 1,050 |

| Utilities & Internet | 210 |

| Groceries | 340 |

| Transportation | 180 |

| Insurance | 120 |

| Phone Subscription | 45 |

| Streaming Services | 38 |

| Dining & Coffee | 210 |

| Gym Membership | 55 |

| Savings Contribution | 400 |

| Miscellaneous Expenses | 260 |

| Total Expenses | 2,908 |

Net Monthly Cash Flow

The monthly cash flow balance is calculated using the following formula:

\text{Net Cash Flow} = \text{Total Income} – \text{Total Expenses}

Result

| Financial Indicator | Amount (£) |

|---|---|

| Total Income | 3,450 |

| Total Expenses | 2,908 |

| Net Cash Flow | 542 |

What This Cash Flow Statement Reveals

At first glance, the financial situation appears healthy.

The individual generates a positive monthly cash flow of £542, meaning expenses remain below total income. This surplus creates financial breathing room and allows savings capacity to grow progressively over time.

However, the statement also reveals several important details that might otherwise remain unnoticed.

Housing Consumes a Significant Share of Income

Rent alone represents nearly one-third of monthly earnings. While this remains relatively common in many UK cities, it reduces flexibility for long-term savings and investment growth.

The dashboard makes this immediately visible.

Small Lifestyle Expenses Add Up Quietly

Dining, coffee, subscriptions, and miscellaneous spending together exceed £500 per month.

Individually, these expenses may feel insignificant. Collectively, they represent a meaningful portion of available liquidity.

Without a cash flow statement, this pattern would likely remain underestimated.

Savings Are Treated Like a Real Expense

One positive aspect of this example lies in the inclusion of savings as a fixed monthly category.

Many people attempt to save only after spending. Financially stable individuals often reverse the logic: savings become part of the monthly structure itself.

This subtle habit changes long-term financial outcomes dramatically.

What Good Cash Flow Actually Means

A positive cash flow does not necessarily mean wealth. It means financial balance remains under control.

Good personal cash flow usually reflects several healthy financial characteristics:

- Expenses remain lower than income

- Emergency savings become possible

- Unexpected bills create less pressure

- Debt dependence decreases

- Financial anxiety gradually reduces

- Long-term planning becomes more realistic

The goal is not perfection.

The goal is visibility and sustainability.

Even a modest positive cash flow maintained consistently can improve financial stability significantly over time.

How to Read a Personal Cash Flow Statement Properly

Many people focus immediately on the final balance. In reality, the most valuable insight often comes from the categories themselves.

A strong cash flow review should analyze:

Fixed Expenses

These include:

- rent

- insurance

- internet

- subscriptions

Fixed expenses determine the minimum financial pressure each month.

Variable Expenses

These include:

- food

- entertainment

- shopping

- transport

- dining

Variable costs usually contain the greatest optimization potential.

Savings Capacity

A strong cash flow statement reveals whether savings are:

- intentional

- irregular

- absent

- improving

This area often becomes the clearest indicator of long-term financial resilience.

Why Excel Works So Well for Cash Flow Management

Despite the popularity of financial apps, Excel remains one of the strongest tools for personal cash flow analysis.

The reason is simple: visibility.

A well-designed Excel dashboard centralizes:

- income tracking

- categorized expenses

- automatic calculations

- monthly summaries

- financial charts

- balance indicators

Everything remains visible in one structured environment.

Unlike many mobile apps, Excel also provides greater flexibility and customization. Users can adapt categories according to lifestyle, profession, or financial goals.

For freelancers, families, students, or entrepreneurs, this flexibility becomes extremely valuable.

How the One-Page Excel Model Is Structured

The personal cash flow template created for this example includes:

- Financial summary cards

- Income tracking section

- Expense categorization

- Budget versus actual comparison

- Automatic balance calculations

- Visual cash flow indicators

- Integrated charts

- One-page dashboard layout

The objective behind the design was simplicity combined with professional financial readability.

Instead of feeling like accounting software, the workbook feels closer to a modern financial control center.

Why Financial Visibility Changes Behavior

One of the most interesting effects of personal cash flow tracking is psychological.

Once spending becomes visible, habits begin changing naturally.

People often become:

- more conscious of recurring expenses

- more deliberate before impulsive purchases

- more realistic about savings goals

- more aware of financial patterns

This transformation rarely comes from pressure alone.

It usually comes from clarity.

A cash flow dashboard creates that clarity by transforming scattered transactions into a readable financial story.

: Investment, Taxation, and Property Management")